Can DAOs Bolster Shareholder Activism?

DAOs can improve corporate governance and empower activist investors to push for change.

In 2014, investor Mark Mobius declared: “Shareholder activism is not a privilege—it is a right and a responsibility.” Essentially, Mobius believed investors ought to be actively involved in company decision-making and use their power to bring about positive change in corporate structures.

Shareholder activism is hardly a new concept. For example, activist investors like Carl Icahn attracted significant attention in the 80s for aggressively pushing for change at portfolio companies.

Shareholder activism has become more popular in recent years, as investors find ways to coordinate and express their views on company issues. Today, activist investors promote positive changes, such as greater institutional commitment to environmental sustainability and diversity and inclusion, financial transparency, and more.

[

[However, the flawed nature of modern corporate governance limits the effectiveness of shareholder activism. Problems such as centralization of decision-making and inadequate participatory mechanisms reduce investor capacity to have their voice heard in corporate settings.

Decentralized autonomous organizations (DAOs) are a new class of institutions that democratize corporate governance. DAOs operate on peer-to-peer protocols (like blockchains) and abandon hierarchical structures in favor of vertical power distribution. With their decentralized nature, DAOs can empower investors and create favorable conditions for shareholder activism.

But, before we go further, let's look at shareholder activism in detail.

What is Shareholder Activism?

According to Investopedia, a shareholder activist is "a person who attempts to use their rights as a shareholder of a publicly-traded corporation to bring about change within or for the corporation."

The objectives of shareholder activists can vary between the financial (increasing investor dividends) and the non-financial (promoting employment diversity). Whatever the motive, shareholder activism is a major tool for investors to express their views on matters concerning a company.

Mark Mobius, whom we earlier quoted, said of shareholder activism:

"When we invest in a company, we own part of that company and we are partly responsible for how that company progresses. If we believe something is going wrong with the company, then we, as shareholders, must become active and vocal."

[

[Shareholder activism exists because investors cannot always trust company management to act in their best interests. This problem is captured in a strand of political-economic theory known as the "principal-agent problem."

In a principal-agent arrangement, the agent is allowed to make legally binding decisions on behalf of the principal. However, a problem occurs when the interests of the agent aren't aligned with those of the principal. Rogue agents may use their proxy power to authorize decisions that benefit them at the expense of principals.

The principal-agent problem is often on full display in companies where the agent (an elected board of directors) may be at odds with the principal (shareholders). In absence of effective checks, company directors might pursue policies that harm investor interests.

Shareholder activism prevents corporate management from running rampant and executing selfish action (like taking fat compensation packages). However, modern-day shareholder activists need better tools if they are to successfully force change.

The Many Problems of Traditional Corporate Governance

In most cases, investors looking to participate in company decision-making have to wait until the Annual General Meeting (AGM). The AGM is a yearly ritual with the outlined purposes of providing up-to-date information on company activity, enabling discussion, and facilitating voting on important decisions, like mergers or appointments.

AGMs are ideal for shareholder activists because it provides a forum to air concerns and, more importantly, allow them to table or vote on proposals. However, modern-day AGMs fail to deliver on their promises and stifle shareholder participation.

[

[For starters, the limited timeframe of these yearly meetings makes it impossible for an extended discussion on issues. With mere hours to cover a large agenda, activist investors may be prevented from sparking a debate around pressing matters.

We also have the problem of logistics. Not every investor is able—or willing—to travel miles to a company's HQ to sit through a half-day meeting. Doing so may be sensible for large shareholders, but smaller shareholders may deem the cost too high, leading to massive declines in turnout at shareholder voting sessions.

Companies have tried to solve this problem by introducing proxy voting. Here, investors receive documents outlining issues under consideration, before the meeting. They can choose to vote on these proposals through mail or via the agreed electronic system.

However, proxy voting has flaws. For instance, there's no way for shareholders to verify if votes were correctly counted and ballot results represent the majority's wishes. The notorious case of Procter & Gamble vs Nelson Peltz illustrates this point:

On the heels of its 2017 shareholder meeting, Procter & Gamble announced that shareholders had voted to reject activist investor Nelson Peltz's bid to join the company's board of directors. However, an independent audit disputed P&G's claim and instead awarded the victory to Peltz, leading to the latter's appointment to the board.

[

[Scenarios like the one described above discourage well-meaning investors from exercising their rights as part owners of a company.

We have seen the major problems with modern-day governance, namely:

- Annual shareholder meetings are limited avenues for discussion due to their short duration

- Logistical costs (time, travel, effort) prevent shareholders, especially retail investors, from participating in meetings

- Proxy voting systems are susceptible to mismanagement and may disenfranchise voters

These problems exist because the thinking around companies and governance has remained unchanged for years. For example, article 70 of the UK's 1856 Joint Stock Companies Act states:

"Once at the least in every year the directors shall lay before the company in general meeting a statement of the income and expenditure for the past year, made up to a date not more than three months before such meeting."

What's surprising here is that sections of the 2006 UK Companies Act contain very similar provisions. These two laws may have been enacted centuries apart, but they share the same flawed thinking.

Improving corporate governance and enhancing shareholder activism in corporations requires novel solutions that empower stakeholders and facilitate transparent decision-making. As Albert Einstein noted, "we cannot solve our problems with the same thinking that created them."

This is where DAOs come into the picture.

Why Shareholder Activism Needs DAOs

A DAO is a collective of individuals who pool resources together to achieve specific objectives. This could be governance (Aragon), provision of financial services (MakerDAO), or in the case of BanklessDAO, media production and education.

DAOs are like companies, except they operate differently. Instead of issuing shares, a DAO sells tokens to prospective members (investors). These tokens confirm holders' membership of the DAO and empower them to participate in governance.

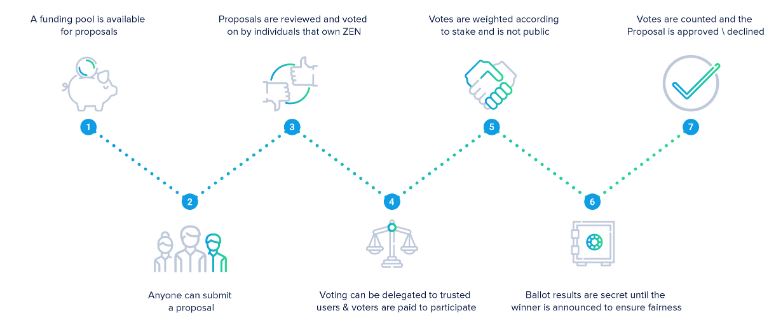

In a DAO, power is distributed across the membership. Every decision must be ratified by the majority of token holders, and no entity can arbitrarily make decisions on behalf of others. Moreover, any member can initiate proposals and seek support from their colleagues.

The rules governing a DAO are encoded into a smart contract and recorded on a transparent and immutable blockchain, preventing any alterations (except when agreed on by the majority). Voting is conducted on-chain, with DAOs allowing stakeholders to cast their votes in an open, decentralized, and secure process.

An example DAO governance process. [Image source]

An example DAO governance process. [Image source]

DAOs solve the principal-agent problem by distributing decision-making power across board. There is no board of directors or CEO calling the shots and pulling the strings for private benefits.

More importantly, DAOs streamline corporate governance and make it easier for investors to initiate or weigh in on proposals. DAOs are location-agnostic institutions and mostly operate through online forums and social networks like Discord. This reduces participation barriers, promoting higher stakeholder engagement in discussion and decision-making.

Besides, DAOs encourage members to submit proposals and give feedback regularly—which means no one has to wait months to table important matters before other stakeholders.

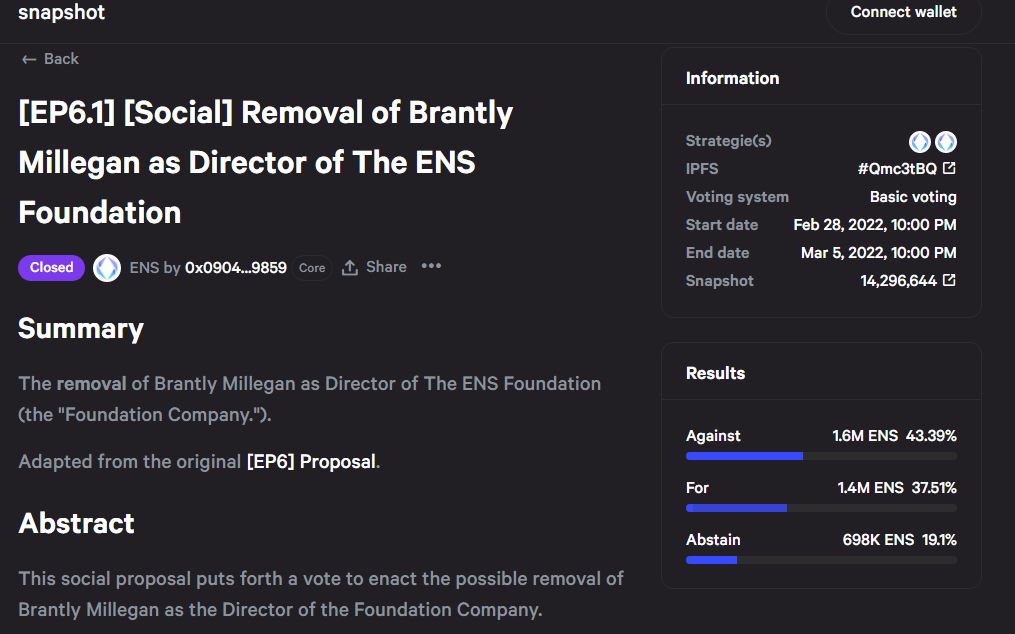

The case involving the Ethereum Name Service (ENS) and its Director of Operations Bryant Millegan is a good example of how DAOs make it easier to call for changes in an organization.

After Millegan was accused of homophobia and misogyny over a series of resurfaced tweets, DAO members initiated a proposal for his removal. Here's a screenshot showing the final results of that proposal:

Now, Millegan eventually held on to his position because the majority voted in his favor. But to focus on the failure to remove him is to miss the forest for the trees.

In a traditional organization, a proposal to remove a high-ranking member would've been a drawn-out process doomed to fail. Or, the decision would've been placed in the hands of a board whose decision may fail to reflect the majority's wish.

However, the ENS DAO's flexible governance structure allowed members to initiate a proposal for change. More importantly, it allowed the entire community to coordinate and express their position on the issue seamlessly.

This is why DAOs matter for activist investors.

Finally, it's important to note that the use of on-chain voting in DAOs increases the integrity of shareholder voting. Thus, it becomes difficult for the management to manipulate results to block activist efforts, as P&G did with Nelson Peltz.

Already, voting tools like Snapshot and Tally ease voting on proposals for DAO participants. Since blockchain transactions can be viewed by anyone, voters can verify results for themselves. And cryptographic security mechanisms make information stored on blockchains immune to alteration.

Why Don't We Just DAO It?

The idea of using blockchain technology to improve corporate governance has old origins. In his 2016 Council of Institutional Investors Keynote Speech, Vice Chancellor J. Travis Laster called modern shareholder voting a 'daisy-chained system of share ownership', describing blockchain technology as a "superior external solution" to problems confronting corporate governance.

While early experiments at mixing company ownership with blockchains, such as The DAO), failed—the industry has matured since then. Today, there are more DAOs than ever, bringing together people from different backgrounds to coordinate and produce value.

If applied correctly, DAOs have the potential to give power back to investors and strengthen their capacity to positively influence company policies. Shareholder activism won't be limited to hedge funds and deep-pocketed investors anymore; retail investors, too, can make their voices heard on issues.

There's still a long road before DAOs become mainstream and provide these benefits. However, if the last years have shown us anything, it's that transformation is starting to happen quickly. With time, DAOs may replace traditional companies—and shareholders will be better off for it.

Cover image courtesy of Financial News